The $7 Cost of Sending $100: Why I’m Obsessed with Payment Rails

When I tell people I’m building a payment infrastructure company, they usually say, "Oh, like PayPal?"

No. Not like PayPal.

PayPal is an application. It sits on top of existing rails the banking system, credit card networks, and stable governments. In the US and Europe, those rails are old, but they work. In Africa, in many corridors, the rails are fragmented, expensive, or simply don't connect.

Let’s talk about the "6% Gap."

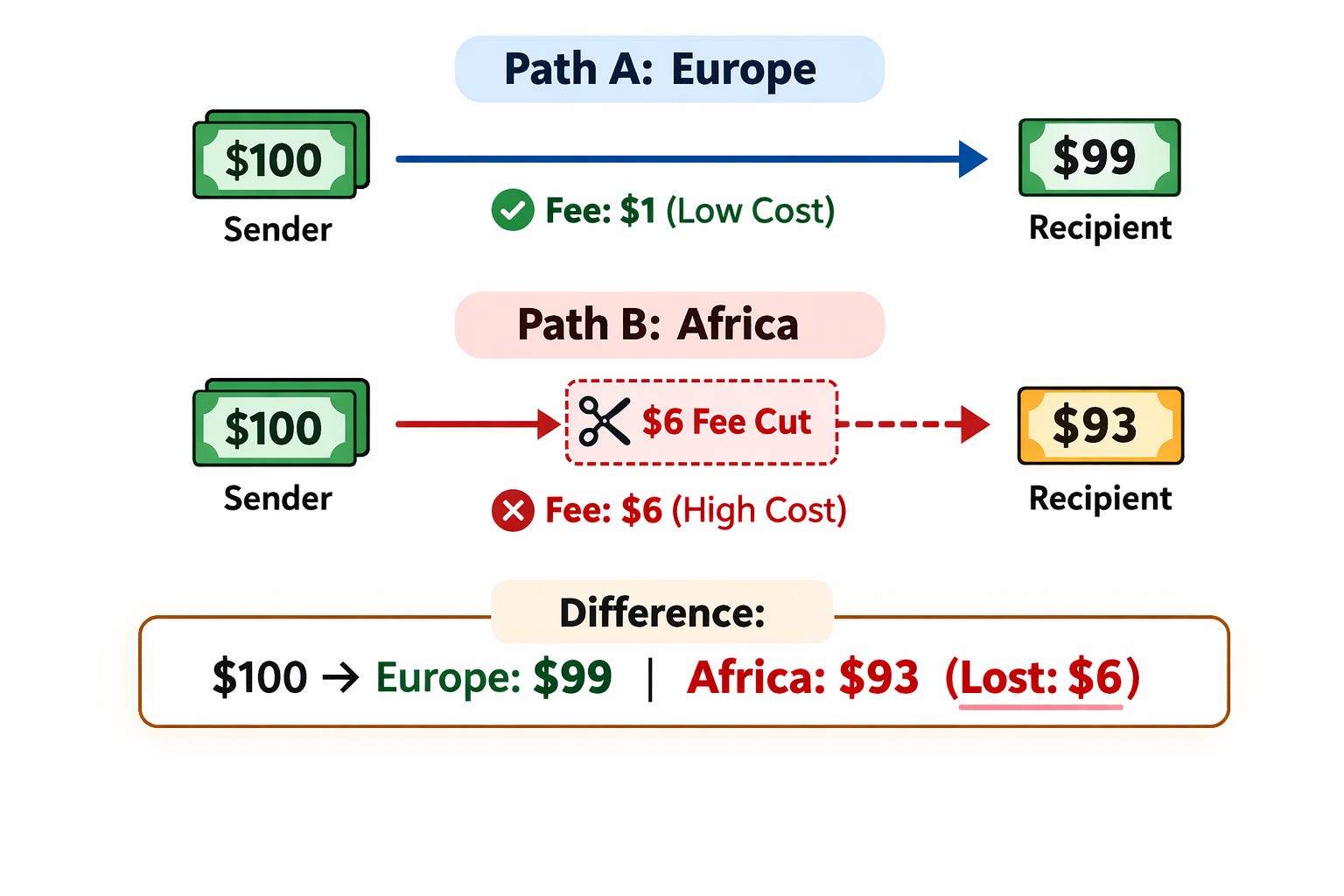

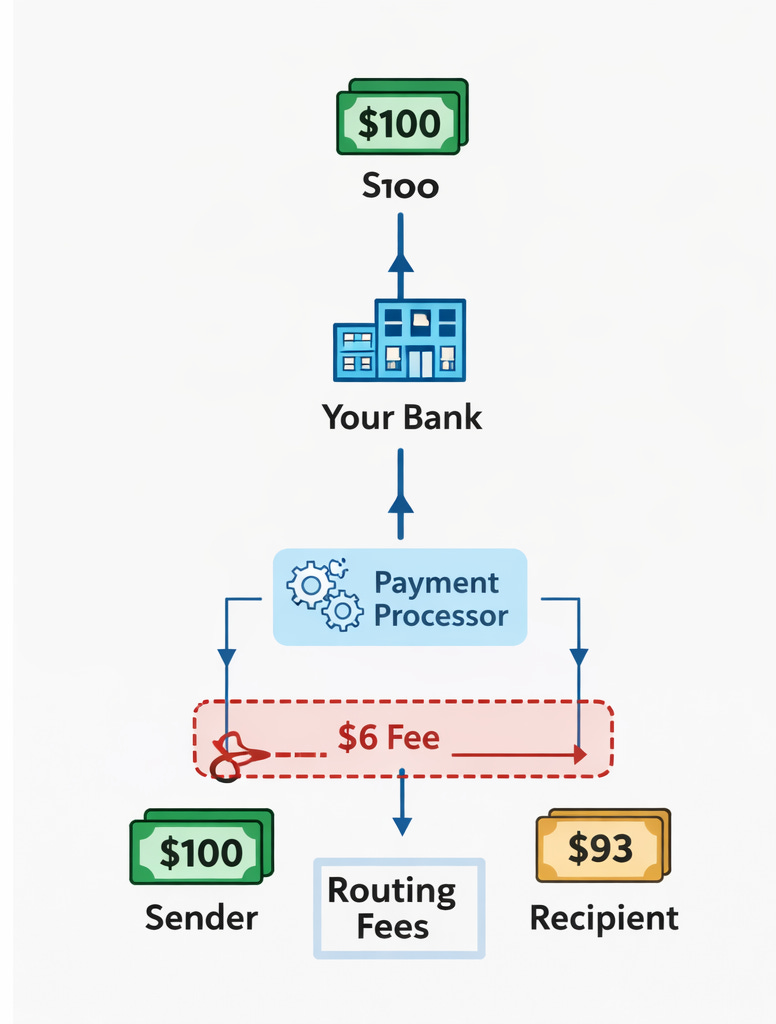

The $31 Billion Friction

Sending money from Nigeria to Kenya involves:

1. Converting NGN to USD (losing money on the spread).

2. Waiting 3-5 days for compliance checks (SWIFT system delays).

3. Converting USD to KES (losing money again).

4. Paying intermediary bank fees.

The result: The recipient gets ~$93. The $7 loss isn't a "service fee." It’s a tax on a broken system.

My Cybersecurity Lens

In my previous life, I looked for vulnerabilities. The biggest vulnerability in African commerce right now isn't hacking it's friction. Friction causes users to seek informal channels (like the parallel market) which exposes them to fraud. Friction kills businesses that operate on thin margins.

At 1APP, we aren't building a pretty interface and calling it a day. We are building the direct bridges between mobile money (M-Pesa), bank accounts, and wallets across 18 countries. We are standardizing the compliance layer so that a transaction doesn't have to stop in London or New York just to go from Lagos to Nairobi.

We are not solving a "tech problem."

We are solving an "infrastructure problem."

The app you see on the phone is just the tip of the iceberg. Underneath, we are moving mountains so you don't have to feel the weight.

The Vision:

Seamlessness. When you send money, you shouldn't feel the borders. You shouldn't feel the banks. You should just feel the connection.

Tomorrow, I’ll shift gears to a different kind of infrastructure—Healthcare—with MEDLITICS. You might be surprised how similar the problems are.